EdTech Market Size to Grow USD 549.6 billion by 2033 | Growing demand for customized education solutions

The growing adoption of digital technologies in educational institutions worldwide is a key growth factor for the EdTech market. The shift towards online learning platforms, digital content, and interactive teaching tools creates opportunities for EdTech companies to innovate and provide value-added solutions.

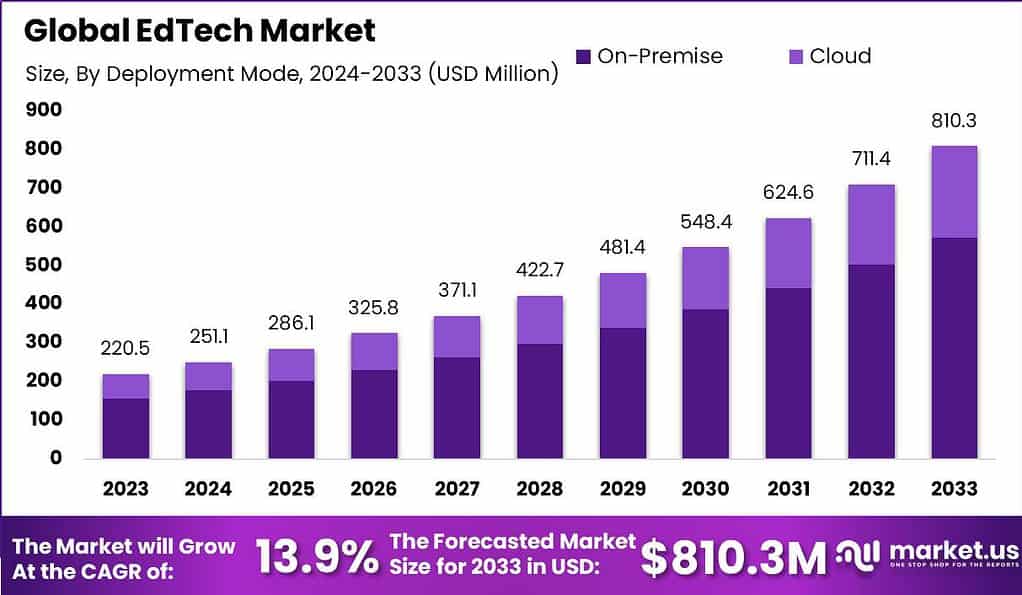

New York, Feb. 13, 2024 (GLOBE NEWSWIRE) -- According to Market.us, The EdTech Market is estimated to be worth USD 146.0 billion in 2023 and projected to be valued at USD 549.6 billion in 2033. Between 2024 and 2033, the market is expected to register a growth rate of 14.2%.

The EdTech (Educational Technology) sector encompasses the application of digital technology to deliver a comprehensive range of educational services and solutions, aimed at enhancing the learning experience, improving access to education, and facilitating the management and delivery of educational content. This sector includes a wide array of products and services, such as online courses, virtual classrooms, learning management systems (LMS), educational software, and digital tools for both students and educators.

The EdTech Market refers to the industry involved in the development, distribution, and utilization of educational technology products and services. It includes companies, startups, educational institutions, government organizations, and other stakeholders contributing to the growth and advancement of EdTech. The market is driven by the increasing adoption of digital learning solutions across educational institutions, from K-12 schools to higher education and professional training.

Tap into Market Opportunities and Stay Ahead of Competitors - Get Your Sample Report Now

Important Revelation:

- Projected Growth: The EdTech market is anticipated to reach a value of around USD 549.6 Billion by 2033, reflecting significant growth from USD 146.0 Billion in 2023, with a projected Compound Annual Growth Rate (CAGR) of 14.2% during the forecast period.

- Hardware Segment: Hardware, including interactive displays, tablets, and laptops, is witnessing significant growth, with an anticipated revenue share of around 60% in 2023, highlighting the increasing adoption of technology-driven teaching methodologies worldwide.

- K-12 Sector Dominance: Within the EdTech market, the K-12 segment dominates with a market share of 40% in 2023, emphasizing the growing adoption of digital tools and interactive learning platforms in primary and secondary education.

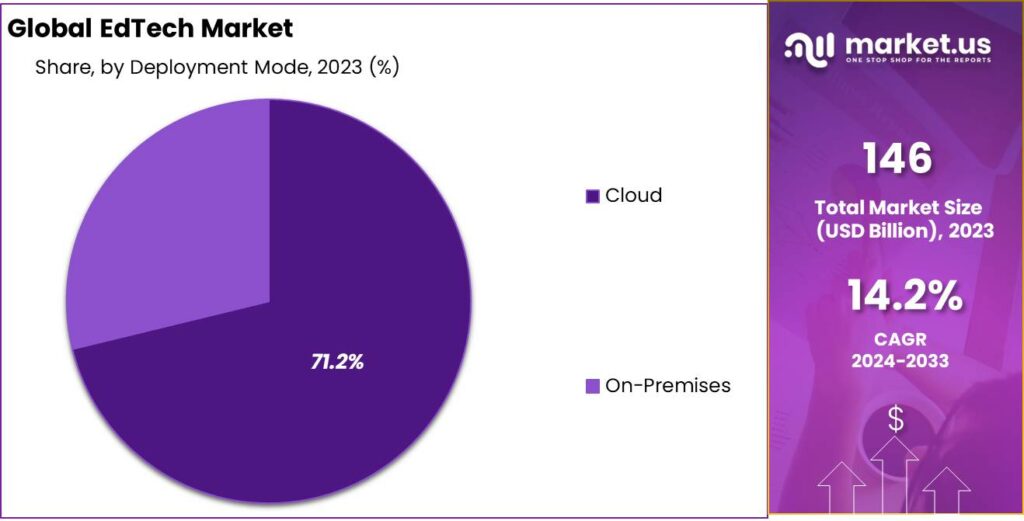

- Cloud Deployment: Cloud-based solutions hold the largest market share, accounting for 71.2% in 2023, driven by their scalability and accessibility, particularly in facilitating remote and hybrid learning models.

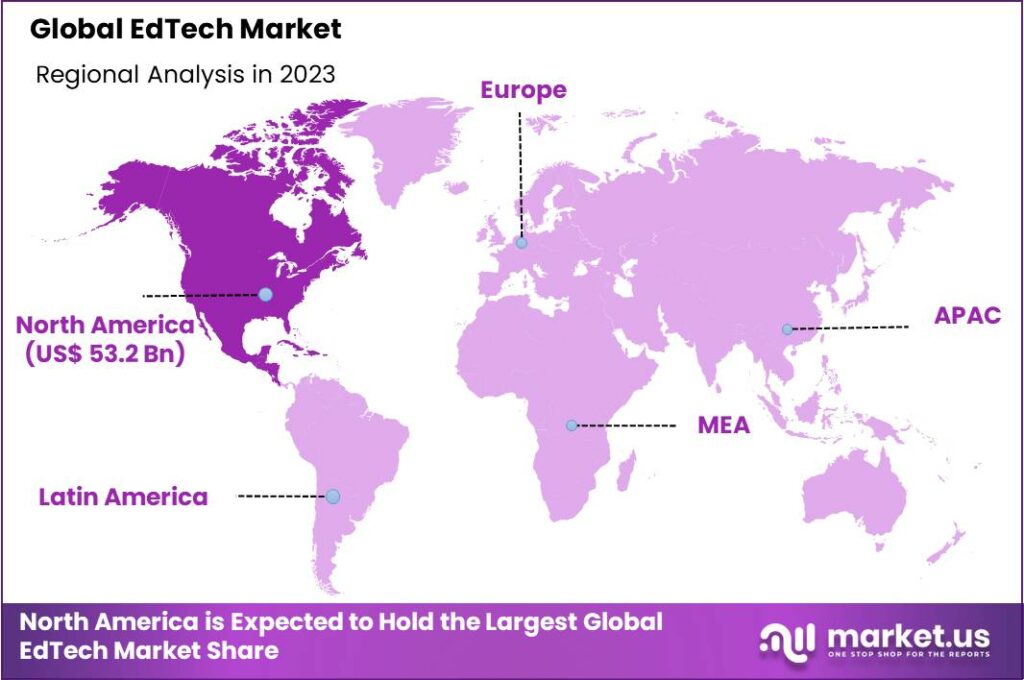

- Regional Analysis: North America dominates the global EdTech market, with a revenue share of 36.5% in 2023, driven by significant investments in the sector. However, Asia Pacific is expected to witness the highest Compound Annual Growth Rate (CAGR) during the forecast period, fueled by the growing use of smart devices and computing.

- Opportunities in Hybrid Learning: Hybrid learning models, combining traditional in-person education with online components, represent a significant opportunity in the evolving landscape of education. This approach allows institutions to leverage the benefits of both physical and virtual learning environments, providing flexibility and personalization.

- Key Players: Prominent players like Coursera, BYJU’S, Chegg, Inc., and Google LLC are driving innovation and influencing the sector’s growth. These players offer diverse educational solutions ranging from massive open online courses (MOOCs) to personalized learning platforms.

Elevate Your Business Strategy! Purchase the Report for Market-Driven Insights: https://market.us/purchase-report/?report_id=101919

Analyst Viewpoint

From an analytical perspective, the growth of the EdTech market can be attributed to several key driving factors. Firstly, the increasing adoption of mobile devices and internet services globally has made educational content more accessible to a broader audience. Secondly, the demand for personalized learning experiences, facilitated by AI and machine learning technologies, is on the rise, as these technologies enable the creation of adaptive learning platforms that cater to the individual needs of learners. Moreover, the integration of AR and VR technologies in educational content delivery is enhancing the interactivity and engagement of learning experiences, presenting significant opportunities for market expansion.

New entrants in the EdTech sector are presented with significant opportunities due to the rising demand for innovative educational solutions. This demand is driven by several key factors including the global shift towards digital learning platforms, the necessity for remote education solutions highlighted by the recent pandemic, and the increasing emphasis on lifelong learning and professional development. The evolving educational landscape, characterized by a growing preference for flexible, accessible, and personalized learning experiences, creates a fertile ground for new players to introduce disruptive technologies and models.

Factors Affecting the Growth of the Global EdTech Market

- Technological Advancements: Continuous innovation in technology, such as artificial intelligence (AI), machine learning (ML), augmented reality (AR), and virtual reality (VR), has revolutionized the EdTech landscape. These advancements enable the development of interactive and personalized learning experiences, enhancing student engagement and comprehension.

- Increasing Internet Penetration: The widespread availability of high-speed internet connectivity, coupled with the proliferation of mobile devices, has democratized access to educational resources. As internet penetration continues to rise globally, more learners can access online courses, digital textbooks, and collaborative learning platforms, fueling the growth of the EdTech market.

- Shift Towards Online Learning: The COVID-19 pandemic accelerated the adoption of online learning solutions as educational institutions worldwide transitioned to remote and hybrid learning models. This paradigm shift underscored the importance of EdTech in delivering seamless and effective learning experiences, driving investment in digital infrastructure and educational technology platforms.

- Rising Demand for Lifelong Learning: In today's knowledge-based economy, continuous learning is essential for career advancement and personal development. EdTech solutions cater to the growing demand for lifelong learning opportunities, offering flexible and accessible educational resources for learners of all ages and backgrounds.

- Personalization and Adaptive Learning: EdTech platforms leverage data analytics and AI algorithms to deliver personalized learning experiences tailored to individual student needs and preferences. By adapting content and pacing based on learner performance and feedback, these platforms optimize engagement and improve learning outcomes, driving increased adoption among educators and learners alike.

Don’t miss out on business opportunities in Market. Speak to our analyst and gain crucial industry insights that will help your business grow.

Top Trends in the Global EdTech Market

Several notable trends are shaping the landscape of the global EdTech market, reflecting evolving educational needs, technological advancements, and shifting learning paradigms. Some of the top trends include:

- Hybrid and Blended Learning Models: With the integration of technology into traditional classrooms, hybrid and blended learning approaches have gained prominence. These models combine in-person instruction with online resources, offering flexibility and personalized learning experiences tailored to individual student needs.

- Artificial Intelligence and Machine Learning: AI and ML technologies are revolutionizing EdTech, enabling adaptive learning platforms, personalized recommendations, and intelligent tutoring systems. These technologies analyze vast amounts of data to provide insights into student performance, optimize content delivery, and enhance learning outcomes.

- Gamification and Immersive Learning Experiences: Gamification techniques, such as badges, rewards, and leaderboards, are being integrated into educational platforms to increase engagement and motivation among students. Similarly, immersive technologies like virtual reality (VR) and augmented reality (AR) are transforming learning environments, offering interactive and experiential learning opportunities across various subjects.

- Microlearning and Bite-sized Content: Microlearning, characterized by short, focused learning modules, is gaining traction as an effective way to deliver information in digestible chunks. EdTech platforms are leveraging microlearning principles to provide on-the-go access to educational content, enabling learners to acquire knowledge quickly and efficiently.

- Social Learning and Collaborative Tools: Social learning platforms and collaborative tools facilitate peer-to-peer interaction, group projects, and knowledge sharing among students. These platforms emulate social networking features to foster community building, collaboration, and peer support, enhancing the overall learning experience.

Regional Analysis:

In 2023, North America emerged as the dominant revenue contributor in the global EdTech market, capturing a significant share of 36.5%. This leadership position can be attributed to several key factors, with one notable driver being the substantial investments made by venture capitalists in the EdTech sector across America. The robust funding ecosystem in North America has fueled innovation and entrepreneurship, fostering the development of groundbreaking EdTech solutions and driving market growth.

The demand for EdTech in North America surged to a remarkable US$ 53.9 billion in 2023, reflecting the region's strong appetite for digital learning solutions and technology-enabled educational experiences. This heightened demand can be attributed to several underlying trends, including the increasing adoption of online and hybrid learning models in educational institutions, the growing emphasis on workforce development and lifelong learning, and the rising demand for personalized and adaptive learning solutions.

Sample Report Request: Unlock Valuable Insights for Your Business: https://market.us/report/edtech-market/request-sample/

Report Segmentation of the EdTech Market:

Type Analysis

In 2023, the hardware segment emerged as the leading contributor to the global EdTech market, representing the largest market share. Moreover, it is anticipated to experience the fastest growth rate during the forecast period. This remarkable performance underscores the critical role of hardware devices in facilitating digital learning experiences and enabling access to educational content and resources.

The dominance of the hardware segment can be attributed to several factors. Firstly, the proliferation of mobile devices, such as tablets, laptops, and smartphones, has revolutionized how students and educators engage with educational content both inside and outside the classroom. These devices serve as platforms for accessing digital textbooks, multimedia resources, and interactive learning applications, empowering learners to explore, collaborate, and create in ways previously unimaginable.

Furthermore, the hardware segment's anticipated 60% revenue share of the global EdTech market in 2023 underscores its significance in the broader education technology ecosystem. As educational institutions and corporate training programs continue to invest in digital infrastructure and technology-enabled learning environments, the demand for educational hardware solutions is expected to soar, driving revenue growth and market penetration for hardware manufacturers and vendors.

Sector Analysis

In 2023, the K-12 segment is projected to assert its dominance in the global EdTech market, capturing a substantial market share of 40%. This significant share highlights the growing adoption of educational technology solutions across primary and secondary education settings, reflecting the increasing importance of digital learning tools in K-12 curricula worldwide.

Several factors contribute to the K-12 segment's dominance in the EdTech market. Firstly, the K-12 education sector represents a vast and diverse market, encompassing millions of students, teachers, and educational institutions globally. As schools and districts seek to modernize teaching and learning practices, they are turning to EdTech solutions to enhance student engagement, personalize instruction, and improve educational outcomes.

Moreover, the K-12 segment's anticipated 40% market share in 2023 reflects its central role in driving revenue growth and market expansion within the EdTech ecosystem. As educational institutions continue to prioritize technology integration and digital transformation initiatives, the demand for K-12-focused EdTech solutions is expected to remain strong, presenting significant opportunities for innovation and investment in the years ahead.

Deployment Analysis

In 2023, the cloud deployment segment emerged as the dominant force in the EdTech market, commanding a significant share of 71.2%. This dominance underscores the widespread adoption of cloud-based solutions across the education technology landscape, driven by several key factors that highlight the advantages of cloud deployment in the EdTech sector.

Firstly, cloud-based solutions offer unparalleled scalability and flexibility, enabling educational institutions to adapt to changing needs and scale their technology infrastructure as demand fluctuates. This scalability is particularly crucial in the context of education, where student enrollment, course offerings, and instructional needs can vary significantly over time.

Secondly, cloud deployment eliminates the need for on-premises infrastructure and hardware maintenance, reducing upfront capital expenditures and ongoing operational costs for educational institutions. By leveraging cloud services, schools, colleges, and universities can redirect resources toward educational initiatives and student support services, maximizing their budgetary efficiency and investment in teaching and learning.

End-User Analysis

The Business end-user segment in the EdTech market primarily caters to corporate training and professional development needs. This segment encompasses a wide range of businesses, including multinational corporations, small and medium-sized enterprises (SMEs), and startups, seeking to enhance the skills, knowledge, and productivity of their workforce through technology-enabled learning solutions.

One of the key drivers for the adoption of EdTech solutions in the business segment is the rapid pace of technological innovation and digital disruption across industries. To remain competitive in the digital economy, businesses must invest in continuous learning and skills development to ensure that their employees are equipped with the latest tools, techniques, and expertise required to excel in their roles.

Additionally, the Business end-user segment benefits from a growing emphasis on talent development and employee engagement as key drivers of organizational success. By investing in professional development initiatives and offering access to online learning platforms, businesses can attract top talent, retain high-performing employees, and foster a culture of continuous learning and innovation.

Plan your Next Best Move. Purchase the Report for Data-driven Insights: https://market.us/purchase-report/?report_id=101919

Top Market Leaders

- Coursera Inc.

- BYJU’S

- Chegg Inc.

- 2U Inc.

- Amazon Inc.

- Blackboard Inc.

- Edutech

- Google LLC

- edX Inc.

- Instructure, Inc.

- Udacity, Inc.

- upGrad Education Private Limited

- Other Key Players.

Recent Developments

1. Chegg Inc.:

- January 2023: Acquired "Thinkful," a coding bootcamp provider, expanding its career-oriented learning offerings.

- March 2023: Launched "Chegg Mathway Expert Q&A," connecting students with live tutors for personalized math help.

- June 2023: Partnered with "Microsoft" to offer Azure cloud computing training courses on its platform.

2. Blackboard Inc.:

- February 2023: Launched "Blackboard Ally for Brightspace," an accessibility management tool for learning platforms.

- June 2023: Partnered with "YuJa" to integrate lecture capture and video management solutions into Blackboard's learning management system.

- October 2023: Acquired "Edmentum," a provider of digital curriculum and assessment solutions.

3. Google LLC:

- January 2023: Launched "Immersive Stream for Education," enabling educators to create and share virtual field trips and immersive learning experiences.

- October 2023: Partnered with Samsung to bring "Chromebooks Enterprise" to more schools, offering enhanced device management and security features for classroom environments.

- December 2023: Launched "Bard," a large language model, showcasing potential applications in personalized learning and knowledge delivery.

Scope of the Report

| Report Attributes | Details |

| Market Value (2023) | USD 146.0 Billion |

| Forecast Revenue 2033 | USD 549.6 Billion |

| CAGR (2024 to 2033) | 14.2% |

| North America Revenue Share | 36.5% |

| Base Year | 2023 |

| Historic Period | 2018 to 2022 |

| Forecast Year | 2024 to 2033 |

Key Market Segments

By Type

- Hardware

- Software

- Content

By Sector

- Preschool

- K-12

- Higher Education

- Other Sectors

By Deployment

- Cloud

- On-Premises

By End User

- Business

- Consumer

- Other End-Users

By Geography

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Explore Extensive Ongoing Coverage on Technology and Media Reports Domain:

- Payment Processing Solutions Market size is expected to be worth around USD 198 Billion by 2032, growing at a CAGR of 12.00%.

- Cybersecurity Insurance Market is set to reach USD 62.7 billion by 2032, predicted to expand at a CAGR of 18.8% till 2032.

- Digital Identity Solutions Market was valued at US$ 28 Bn and is projected to reach US$ 131.6 Bn by 2032, with the highest CAGR of 17.2%.

- Retail Analytics Market size is expected to be worth around USD 39.6 Bn by 2032 from USD 5.7 Bn in 2022, growing at a CAGR of 22%.

- Data Catalog Market accounted for USD 718.1 Mn in 2022. It is estimated to reach USD 5,235.2 Mn at a CAGR of 22.6% between 2023 and 2032.

- Game-Based Learning Market is expected to reach USD 77.4 bn between 2023 and 2032; register the highest CAGR of 21.6%.

- API Management Market will reach USD 49.9 Billion in 2032, from USD 4.5 Billion in 2022; at a CAGR of 28% during forecast period.

- Electric Vehicle (EV) Charging Infrastructure Market is Set to Attain USD 224.8 Billion by 2032, Expands Steadily at a CAGR of 27.5%.

- Farm Management Software Market was USD 2.60 bn in 2022. It is estimated to reach USD 8.94 bn in 2032, CAGR of 13.5% from 2023-32.

- AI Training Dataset Market was valued at USD 1.9 Billion in 2022. This market is estimated to register the highest CAGR of 20.5%.

- Neuromorphic Computing Market reached USD 4.2 Bn in 2022 and is projected to reach US$ 29.2 Bn by 2032, growing at a CAGR of 22%

- Speech and voice recognition market size is expected to be worth around USD 83 bn by 2032 from USD 14 bn in 2022, grow at a CAGR of 20%

- By 2032, the Satellite Communication market is anticipated to grow at a 9.4% CAGR, having reached USD 182.7 billion.

- Data Center Construction Market size is projected to reach a valuation of USD 453.5 Billion by 2033 at a CAGR of 6.7%.

About Us

Market.US (Powered by Prudour Pvt Ltd) specializes in in-depth market research and analysis and has been proving its mettle as a consulting and customized market research company, apart from being a much sought-after syndicated market research report-providing firm. Market.US provides customization to suit any specific or unique requirement and tailor-makes reports as per request. We go beyond boundaries to take analytics, analysis, study, and outlook to newer heights and broader horizons.

Follow Us On LinkedIn Facebook Twitter

Our Blog:

Global Business Development Team - Market.us Market.us (Powered By Prudour Pvt. Ltd.) Email: inquiry@market.us Address: 420 Lexington Avenue, Suite 300, New York City, NY 10170, United States Tel: +1 718 618 4351 Website: https://market.us/

Legal Disclaimer:

EIN Presswire provides this news content "as is" without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the author above.